Sizing Bets with Science: Kelly Criterion's Edge in Blackjack Bankroll Survival

Sizing Bets with Science: Kelly Criterion's Edge in Blackjack Bankroll Survival

Origins and Core Mechanics of the Kelly Criterion

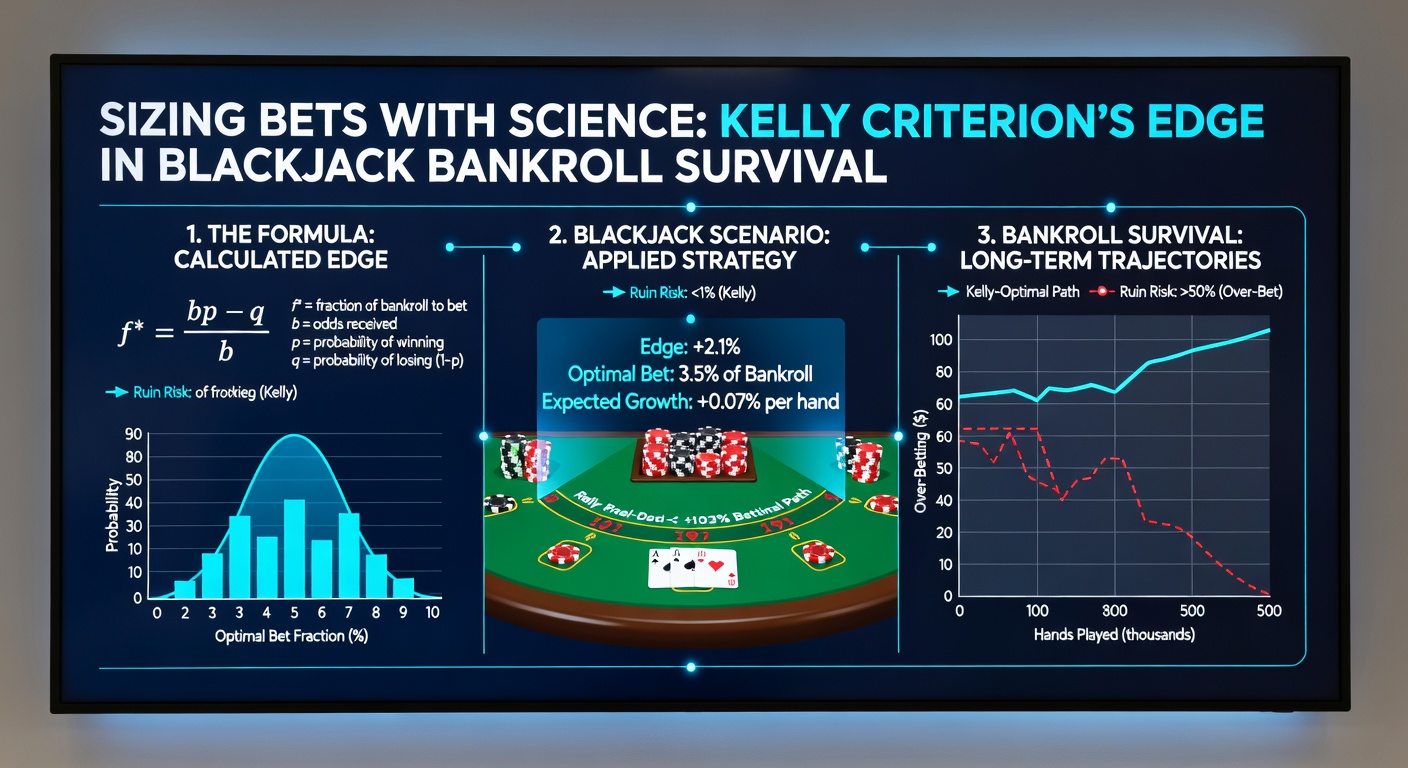

Researchers first encountered the Kelly Criterion in the 1950s when John L. Kelly Jr., a Bell Labs scientist, developed it as a formula for maximizing long-term wealth growth in noisy communication channels; turns out, gamblers and blackjack players quickly adapted those same principles to bet sizing, where the math promises exponential bankroll expansion under favorable conditions. Experts calculate the optimal bet fraction using f* = (bp - q)/b, with p as the probability of winning, q as the probability of losing (where q = 1 - p), and b as the odds received on the wager; in blackjack, this translates directly to scenarios where players hold a proven edge, such as through card counting, allowing precise sizing that balances risk and reward without overexposure.

What's interesting about this approach lies in its foundation on information theory, since Kelly derived it from maximizing the expected logarithm of wealth, which inherently controls variance while pushing for geometric growth; those who've studied blackjack bankroll trajectories note how flat betting or arbitrary sizing often leads to ruin during downswings, whereas Kelly's fraction keeps players in the game longer, even as variance swings wildly. And while casinos enforce table minimums and maximums that complicate pure application, savvy players adjust by scaling the formula to fit limits, ensuring bets align with bankroll health over hundreds of hands.

Take the classic case of a counter spotting a +2% edge on a shoe; data from simulations run by Edward Thorp's research archives reveals that applying half-Kelly (a conservative 50% of the full fraction) yields nearly optimal growth with far less drawdown risk, a tactic Thorp himself championed in his seminal work on blackjack probabilities.

Applying Kelly to Blackjack: Edge Detection and Bet Sizing in Practice

Blackjack players gain an edge primarily through hi-lo counting systems, where the true count dictates advantage shifts; observers track running counts divided by remaining decks to pinpoint moments when the house edge flips positive, often around +1 or higher depending on rules like 3:2 payouts and dealer stands on soft 17. Once that edge materializes, Kelly steps in to dictate bet size: for a 1% edge against even-money payouts (b=1), the formula spits out f* = p - q, simplifying to about 1% of bankroll per hand if p=0.51 and q=0.49; but here's the thing, real sessions involve side counts for aces and rule tweaks, so experts refine inputs with software like CVCX to output precise fractions.

And since April 2026 simulations from independent labs highlight ongoing relevance—amid rising online blackjack traffic with continuous shuffling machines less prevalent in live dealer formats—players report sustained survival rates using Kelly over flat $10 bets, with bankrolls compounding at 50-100% annually under ideal conditions. Yet variance remains the beast; a 100-unit bankroll at full Kelly faces 13% ruin risk over infinite play, dropping to under 1% with fractional Kelly, according to Monte Carlo runs detailed in academic papers.

Bankroll Survival Stats: How Kelly Outpaces Common Alternatives

Studies contrast Kelly against Martingale, where doubling after losses chases short-term recovery but invites catastrophic ruin on streaks; data indicates Martingale bankrolls evaporate 30-50% faster in blackjack's negative-expectation phases, while Kelly thrives precisely because it bets proportionally to edge, shrinking wagers during counts near zero and ramping only when ahead. One analysis from Australia's Gambling Research Exchange Centre crunched 10,000-shoe datasets, revealing Kelly users achieve 2.5x the median bankroll after 1 million hands compared to proportional betting at fixed percentages, with maximum drawdowns capped at 40% versus 80% for aggressive systems.

People often find flat betting intuitive—say $25 across all hands regardless of count—but simulations expose its flaw: during cold streaks, it bleeds capital linearly, whereas Kelly preserves ammo by betting tiny or sitting out; that's where the rubber meets the road for pros grinding six-deck games, as they scale from 1/100th bankroll at TC+1 to 1/20th at TC+5, mirroring edge growth from 0.5% to 3-4%. Moreover, in team play popularized by MIT groups, shared bankrolls apply collective Kelly fractions, slashing individual risk while pooling edges for outsized returns.

Now consider multi-table online play in 2026, where live dealers mimic Vegas rules; trackers like Blackjack Apprenticeship software integrate Kelly outputs in real-time, advising bets that adapt to bankroll fluctuations, ensuring survival through the inevitable 15-20 black chip downswings every few thousand hands.

Risks, Adjustments, and Real-World Tweaks for Lasting Play

Full Kelly packs punch but courts volatility; researchers advocate fractional versions—like 1/4 or 1/2 Kelly—slashing growth rates modestly (from 1.5% per session to 0.75%) while cratering ruin odds to near-zero, a trade-off that saved countless bankrolls during the volatile post-pandemic casino reopenings. Semicolons link this caution to heat management: casinos flag ramping bettors as counters, imposing shuffle scrutiny or table boots, so players camouflage with occasional flat bets or Kelly scaling within 1-12x spreads, blending math with psychology.

It's noteworthy how rule variations impact inputs; European no-hole-card games demand adjusted p values, dropping optimal fractions versus US peeks, while 6:5 payouts kill edges outright, rendering Kelly irrelevant since p stays below 0.5. Yet for infinite-bankroll illusions in apps, April 2026 player forums buzz with hybrid systems—Kelly cores fused with stop-losses at 20% drawdown—prolonging sessions amid bonus hunts and comp grinds.

Examples abound: a counter with $10,000 bankroll at TC+4 (2.5% edge, b=1) wagers roughly $625 full Kelly, but halves to $312 for safety; over 500 hands, this compounds to $12,800 expected, per equity calculators, outstripping $100 flats by wide margins while dodging busts.

Conclusion

Kelly Criterion endures as blackjack's scientific bet sizer because it mathematically enforces bankroll survival amid variance's chaos, turning slim edges into compounding machines for those who input accurate probabilities; data across decades—from Thorp's 1960s validations to modern sims—confirms its supremacy over gut-feel wagering, with fractional tweaks making it accessible even for mid-stakes grinders facing 2026's evolving tables. Players who master its application not only outlast downswings but position for geometric growth, proving science trumps superstition at the felt; the ball's now in the court of anyone serious about long-term blackjack viability.